1031 Exchanges

A Charleston Law Firm’s Concise Summary of 1031 Exchanges. Let’s get some legal formalities out of the way at the very onset. The information provided herein is intended merely as a concise summary of like-kind exchanges under §1031 of the Internal Revenue Code and related tax laws. This article cannot, and therefore does not, reflect any changes in the law that occur subsequent to the publication of this article. It was not designed to provide all restrictions or exceptions that might apply to a taxpayer’s particular circumstance. This article is not a substitute for legal advice. We at Bradshaw & Company, LLC hope that you will find the information informative and useful, and we would be delighted to speak with you to answer any additional questions you may have.

To ensure compliance with requirements imposed by the IRS, Bradshaw & Company, LLC and its attorneys inform all readers of this article that (1) any U.S. federal tax advice contained in this article is not intended or written to be used, and therefore cannot be used, by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer under the Internal Revenue Code of 1986, as amended; (2) any written statement contained in this article relating to any federal tax transaction(s) or matter(s) may not be used by any person to support the promotion or marketing of or to recommend any federal tax transaction(s) or matter(s) addressed in this article; and (3) any taxpayer should seek advice based on the taxpayer's particular circumstances from an independent tax advisor with respect to any tax transaction or matter contained in this article.

No one, without the express prior written permission from Bradshaw & Company, LLC, may use any part of this article in promoting, marketing, or recommending an arrangement relating to any federal tax matter to one or more taxpayers. And so, without any further ado, let’s get started.

Introduction: Two simple questions – Do you own investment, rental, or undeveloped property that would produce a taxable capital gain if you were to sell that property? Would you be willing to reinvest your money in other appreciating real estate in order to avoid paying any immediate capital gain tax on your sale? If the answer to both is “yes,” then consider structuring your sale as a §1031 like-kind exchange.

Stated simply, a §1031 exchange allows you to sell an investment property and then reinvest your sale proceeds in more investment property without incurring immediate federal or South Carolina capital gains tax in the process. This article summarizes this tax advantageous strategy that has enabled millions of investors to grow their real estate portfolios without unnecessary tax erosion.

In selecting the appropriate professionals to structure, coordinate, and finalize your §1031 exchange, your primary concerns should be security, integrity, and professionalism. Although several Charleston attorneys put themselves forth as being able to manage a §1031 like-kind exchange, our team at Bradshaw & Company, LLC brings to the table over 10 years of experience in the like-kind exchange arena as well as highly specialized knowledge in taxation law. Our proven reputation for solid expertise, integrity, and professionalism echoes throughout Charleston’s real estate community. If you are considering structuring your next real estate sale as a §1031 exchange, we urge you to contact us with any questions you may have. We’re confident that you’ll discover what we mean by, “delivering service beyond expectations.”

The Basics: The like-kind exchange is authorized by Section 1031 of the Internal Revenue Code, which provides in part that a property owner who sells his real property (other than his home) and then reinvests the proceeds in ownership of “like-kind property” is able to do so while deferring any capital gains tax – perhaps indefinitely. To qualify as a like-kind exchange, property exchanges must satisfy all of the requirements set forth in the tax code and treasury regulations. Note, however, that the Code’s ''like-kind'' property requirement does not mean “same kind.”

With respect to real estate, “like-kind” simply means real estate that was held for investment or for use in a trade or business. Virtually the only real properties that are not eligible for tax-deferred trades are your personal residence and property owned by a “real estate dealer” such as a home builder or developer. For example, if you own a rental house that you want to exchange for an office building and/or undeveloped land of equal or greater cost and equity, you can do an exchange. You could exchange an industrial warehouse for a golf course or a parking lot for a hotel. Basically, real estate is real estate – so long as it’s not one of your homes or purchased solely for resale.

Parties & Properties: Although it is certainly possible for two parties to “swap” real estate with each other, the overwhelming majority of §1031 exchanges involve multiple parties. At most, you should be aware of five possible parties involved in an exchange. They include:

The Exchanging Taxpayer;

The Third-Party Seller;

The Third-Party Buyer;

The Qualified Intermediary; and

The Exchange Accommodation Titleholder.

The exchanging taxpayer is you. Real estate that you wish to sell in a §1031 exchange is called “Relinquished Property.” Conversely, the real estate that you wish to purchase in a §1031 exchange is called “Replacement Property.” The third-party Buyer and Seller are parties on the other side of a closing table who purchase your Relinquished Property and sell you your Replacement Property respectively. In a straight exchange, the Qualified Intermediary is an unrelated third-party entity whose only purpose is to facilitate the exchange. The Qualified Intermediary provides the professional service of holding all exchange monies in an escrow account during the exchange period in return for a fee. In a reverse exchange, that same unrelated third-party entity is referred to as an Exchange Accommodation Titleholder, because, instead of holding exchange monies, it temporarily holds title to the exchanged real estate until the exchange is complete.

Specific Requirements: The IRS is very strict on taxpayers satisfying the requirements of IRC §1031 and the related Treasury Regulations. The following is a brief list of specific requirements of which you should be aware:

Qualified Property → For purposes of real estate, investment or business property qualifies; exchange property cannot include homes (either primary or otherwise), foreign real estate, or interests in entities such as multi-member limited liability companies or partnerships that may themselves hold U.S. real estate. Such entities, however, can directly exchange their property with other taxpayers.

Holding Period → Currently, no law provides how long you must have held your investment property in order to qualify for tax-deferred treatment. A one-year holding period is commonly used as a rule of thumb, although the longer the better. In the absence of any statutory or judicial guidance, the issue of how long is sufficient turns on your individual tolerance for risk.

Time Limits → Two time limits must be respected when performing a proper exchange. First, you must identify your Replacement Property within 45 calendar days of closing on your Relinquished Property. Second, you must close on the purchase of your Replacement Property within 180 calendar days of the earlier of either closing on your Relinquished Property or the due date of your federal income tax return (including extensions) for the tax year in which the Relinquished Property is transferred. This discussion of time limits applies to reverse exchanges as well, but all references to your Replacement Property and Relinquished Property are reversed. Unfortunately, there are absolutely NO exceptions to these time limits. Even if a deadline falls on a weekend or a legal holiday, there are absolutely NO exceptions to these time limits.

Identification of Replacement Property → Generally, you can identify up to three properties regardless of their fair market values. In the event that you wish to identify more than three properties within the 45-day period, additional rules apply, which are more fully addressed in the discussion of Delayed Exchanges.

Related Parties → Generally, if you are selling your Relinquished Property to an unrelated party, then you may not acquire your Replacement Property from a related party unless the related party is also exchanging pursuant to §1031. On the other hand, if the Relinquished Property is transferred to a related party, then the related party must own it for a minimum of 2yrs prior to disposing of it. Similarly, you may do a two-party swap with a related party so long as both of you hold your respective Replacement Properties for at least two years. For purposes of this requirement, related parties include parents, siblings, children, spouses, or an entity in which you or a relative owns more than 50%.

Constructive Receipt → Treasury Regulations provide that income, even though it is not actually in your possession, will be deemed to have been “constructively” received if it is credited to your account, set apart for you, or otherwise made available so that you can draw upon it at any time. If you actually or constructively receive any proceeds from the disposition of your Relinquished Property, part of the transaction will be re-characterized as a sale rather than an exchange. The Internal Revenue Code provides a number of complicated rules that must be followed to avoid a finding of constructive receipt. Bradshaw & Company, LLC can protect you from this potential problem by carefully drafting all documents necessary to structure your exchange and through the use of experienced qualified intermediaries.

Maximizing the Amount Deferred → Generally, to avoid any immediate capital gains tax upon completion of your exchange, the cost of (and your equity in) your Replacement Property must be equal to or greater than the cost of (and your equity in) your Relinquished Property. Of course, you can still do an exchange if the fair market value of your Replacement Property is less than the fair market value of your Relinquished property, but there will be some tax consequences.

Types of Exchanges: Exchanges are generally structured in one of five ways, including:

Two-Party Exchanges;

Simultaneous Exchanges;

Delayed Exchanges;

Reverse Exchanges; and

Split Exchanges.

The particular structure of any exchange depends on the circumstances surrounding each taxpayer and his or her objectives. Although the Two-Party Exchange and the Simultaneous Exchange still arise, neither is very common today. Illustrations of these two structures can be gleaned from the discussion of Reverse Exchanges. For practical purposes, however, this article focuses solely on the last three structures: the Delayed Exchange, the Reverse Exchange, and the Split Exchange.

The Delayed Exchange

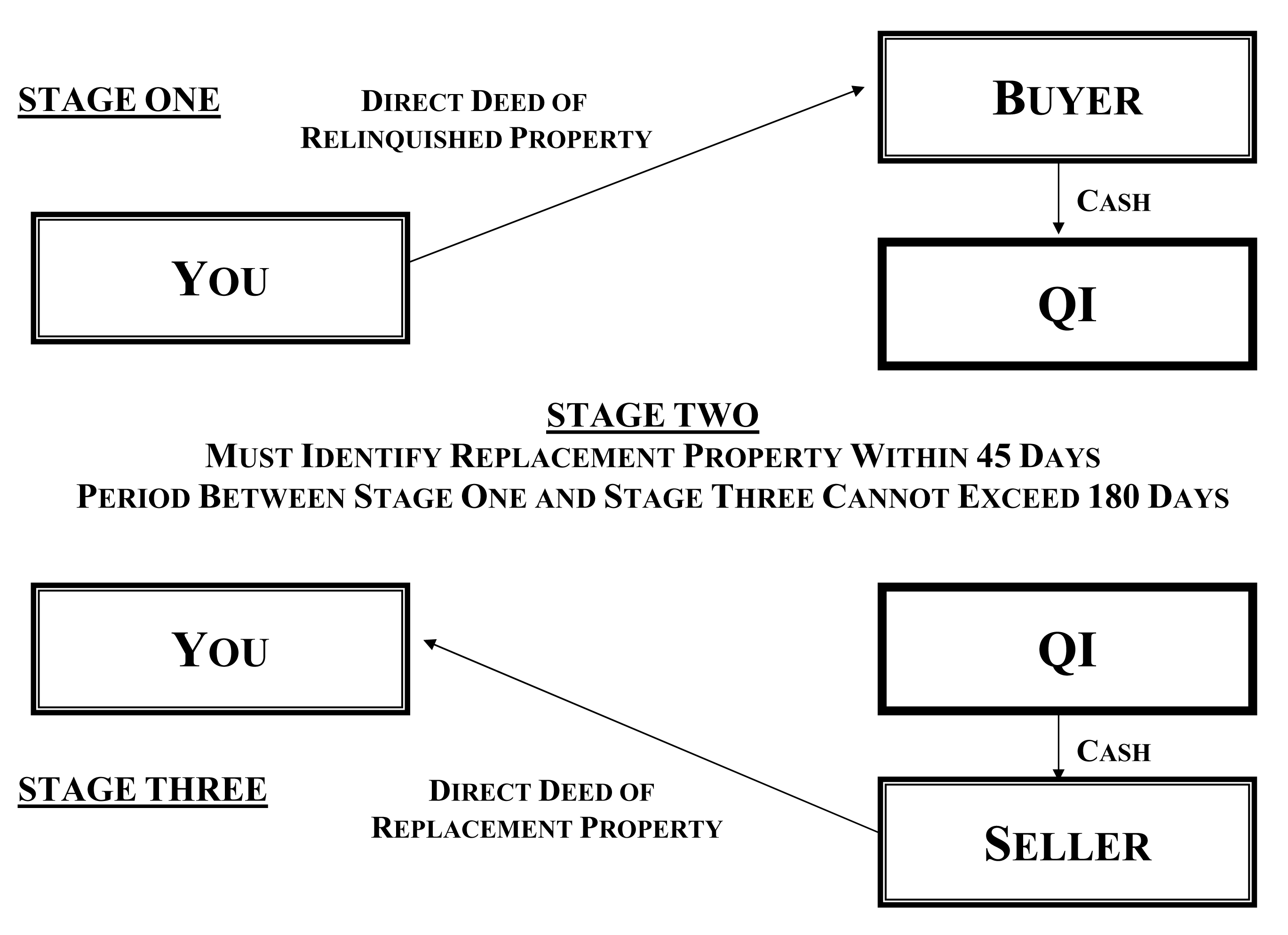

Currently, the Delayed Exchange is perhaps the most common §1031 exchange structure. The exchange occurs in three fundamental stages.

Currently, the Delayed Exchange is perhaps the most common §1031 exchange structure. The exchange occurs in three fundamental stages.

STAGE ONE: Sale of the Relinquished Property. Before you close on the sale of your Relinquished Property, you would retain a law firm such as Bradshaw & Company, LLC who would prepare all documents necessary for your exchange. These documents generally include an exchange agreement, an assignment of sale contract, a form to identify your Replacement Property or Properties, and closing instructions if Bradshaw & Company, LLC does not also handle the real estate closing for you.

At closing, you will assign your rights to the purchase and sale contract to the Qualified Intermediary (QI). The net sales proceeds from the sale of your Relinquished Property would be deposited by the QI and held until the subsequent closing of your Relinquished property. Once the funds are deposited with the QI, access to the funds is restricted for the remainder of the exchange period.

STAGE TWO: Identification of the Replacement Property. Within 45 calendar days of the closing of your Relinquished Property, you must identify your Replacement Property (or Properties) using the form we provided to you. There are additional rules for how many properties you can identify in an exchange. If at the end of the 45-day identification period you have identified more properties than permitted by IRC §1031, it is treated as if no property was identified and the exchange will be disallowed. The following three identification rules apply:

3 Property Rule: You can identify up to three different parcels of real estate no matter what their fair market value may be.

200% Rule: You may identify more than three different properties as long as the aggregate fair market value does not exceed 200% of the fair market value of all of your Relinquished Property (or Properties).

95% Rule: You can identify any number of properties without regard to the value provided 95% of the value of the identified properties is ultimately acquired in the exchange.

STAGE THREE: Purchase of the Replacement Property. Within 180 calendar days from either the closing of your Relinquished Property or your tax filing date (whichever occurs first), you must acquire your Replacement Property from your list of “identified” Replacement Properties. At the closing for the purchase of your Replacement Property, you will again assign the purchase and sale contract to the QI, who then will purchase the Replacement Property using the sale proceeds held in escrow from the sale of your Relinquished Property. The QI simultaneously transfers the Replacement Property to you by a direct deed from the Seller.

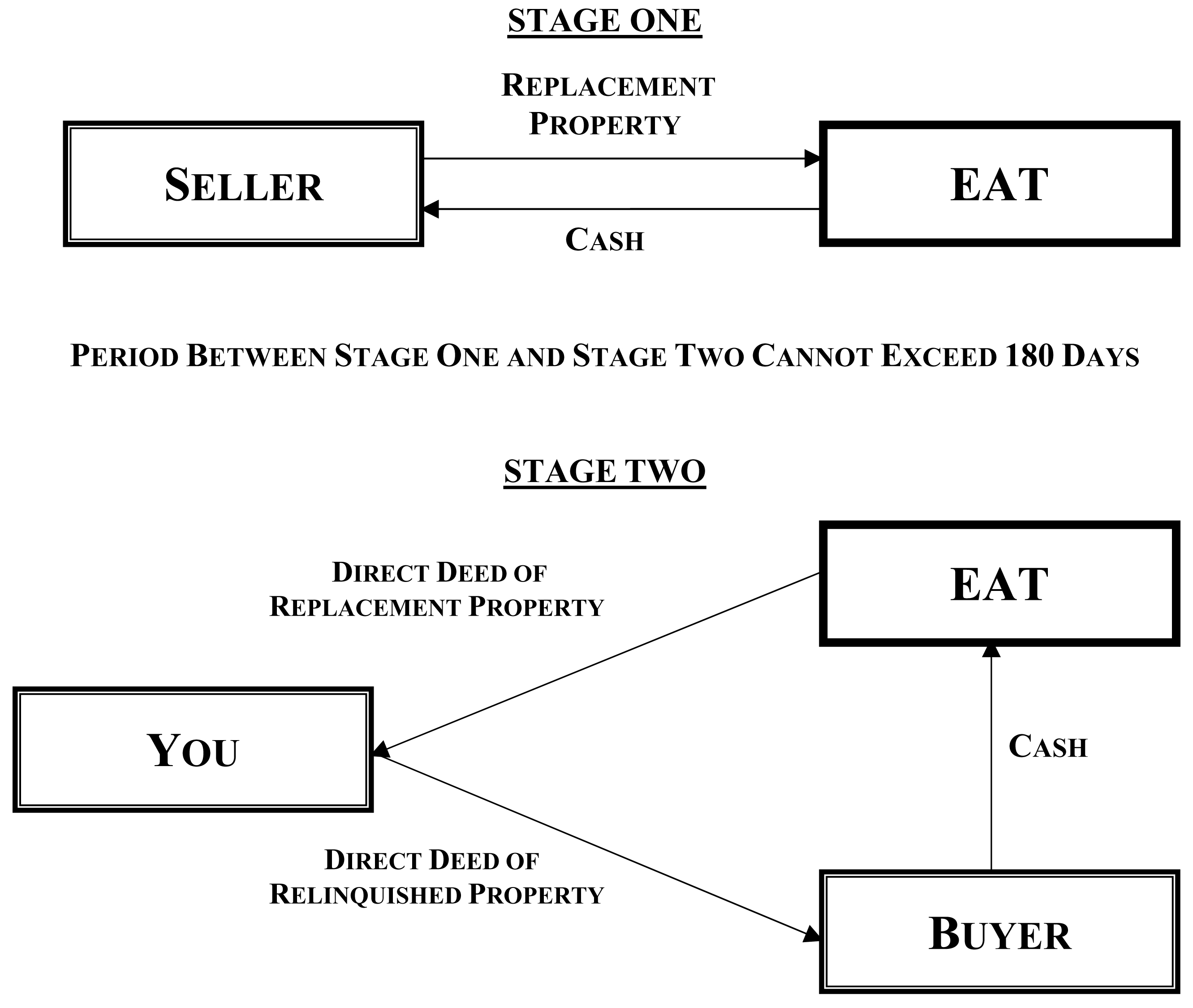

The Reverse Exchange

The Reverse Exchange has been growing in popularity since the IRS formally acknowledged the transaction on September 15, 2000. The Reverse Exchange is essentially the same as the Delayed Exchange except that you would acquire your Replacement Property prior to the sale of your Relinquished Property. This situation often arises when you find a desirable Replacement Property that may not remain available until you’re able to sell your Relinquished Property. Generally, all of the rules discussed above still apply. One difference is that the Qualified Intermediary used by Bradshaw & Company, LLC temporarily holds the title to real estate used in the exchange and is now referred to as the Exchange Accommodation Titleholder (“EAT”). There are two varieties of Reverse Exchanges, the first involves parking title to the Replacement Property with the EAT before the exchange, and the second involves parking title to the Relinquished Property after the exchange. Bradshaw & Company LLC

Reverse Exchange – Relinquished Property Parked

DOWNLOAD THE May 3, 2015 NEWSLETTER HERE

No matter which property is parked, the EAT will enter into a management agreement or master lease with you to allow you to manage or lease the property for the duration of the parking period. Additionally, in a transaction involving financing, the EAT may become the borrower under a non-recourse loan; upon the expiration of the exchange period or the sale of the Relinquished Property and subsequent transfer of the Replacement Property to you, you will then assume the loan. Likewise, the EAT will require hazard and liability insurance during the holding period.

Within 5 business days after the EAT acquires title to the parked property, you and the EAT must enter into a written qualified exchange accommodation agreement. You then will have 45 calendar days to identify one or more Relinquished Properties. The same three identification rules that apply to delayed exchanges (discussed previously) apply to reverse exchanges. Written identification of the Relinquished Properties must be delivered to the EAT or to another party to the exchange. The exchange must be completed within 180 calendar days (i.e., the Relinquished Property must be conveyed to a third party Buyer and the Replacement Property must be conveyed to you). Once again, there are NO exceptions to these deadlines.

The Split Exchange

In a split exchange, a reverse exchange is combined with and followed by a deferred exchange. Of course, a number of complex rules surround the proper structuring of a split §1031 exchange. While a comprehensive discussion of these rules and all moving parts is beyond the scope of this article, we encourage you to contact us if you would like to learn more about split exchanges and to determine whether it would be appropriate for your next transaction.

The “Build to Suit” Exchange

An extremely common question in the Charleston market involves improvements and new construction of Replacement Property. In its most common application, this is a §1031 exchange in which you purchase raw land as Replacement Property and then construct improvements on the land within 180 days of the sale of the Relinquished Property. If properly structured, the improvements can qualify with the raw land as Replacement Property. This type of transaction is very complex and should not be pursued without the involvement of both an experienced tax professional and a sophisticated Qualified Intermediary.

Tax Consequences: Here’s where the proverbial rubber hits the road. Determining the tax consequences of exchange begins with an understanding of the terms: “adjusted basis,” “capital gain,” “boot,” and “capital gain tax.”

Adjusted Basis → In most situations, the starting point for determining an adjusted basis is the amount you originally paid for your Relinquished Property. You then need to adjust this cost amount by adding the sum total of all capital improvements you’ve made to the property since you’ve owned it, then subtract any depreciation taken on the property during that same period of your ownership. Thus, if you originally purchased your Relinquished Property for $800,000, later spent $200,000 in renovations and other capital improvements, and have taken $50,000 worth of depreciation deductions for the building on the property, your calculation would look something like this:

$800,000 | Cost Basis in Relinquished Property | |

+ | $200,000 | Capital Improvements |

– | $50,000 | Depreciation Deductions |

$950,000 | Adjusted Basis |

Capital Gain → The estimated capital gain calculation involves two steps:

First, subtract the adjusted basis from the sales price of your Relinquished Property.

Second, subtract the permissible costs of selling your Relinquished Property.

What constitutes permissible and non-permissible expenses and closing costs can vary by geographic region based on common practices, local standards, and customs. In Charleston, South Carolina, permissible expenses and closing costs usually include:

Owner’s Title Insurance Premiums,

Escrow Fees,

Broker’s Commissions,

Finder’s Fees,

§1031 Qualified Intermediary (EAT) Fees,

Transfer Taxes,

Recording Fees,

Legal Counsel/Attorney Fees, and

Tax Advisor/Accountant Fees.

Non-Permissible Expenses and Closing Costs, however, usually include:

Financing costs such as loan fees, loan points, appraisal fees, mortgage insurance premiums, lender's title insurance policy premiums, and other loan processing fees and costs;

Property taxes;

Prorated or prepaid rents;

Insurance premium payments (e.g., hazard, flood);

Security deposits;

Association dues;

Utility charges; or

Payoff of credit card balances.

Thus, your capital gain calculation may look something like this:

$1,450,000 | Contract Sales Price | |

– | $950,000 | Adjusted Basis |

– | $20,000 | Permissible Expenses & Closing Costs |

$480,000 | Capital Gain |

Boot → Although an unusual term, “boot” essentially means any value that you receive either actually or constructively at closing. Boot is taxable. You need to become familiar with two varieties of boot – “cash boot” and “mortgage boot.”

“Cash boot” is cash or any other value received in the transaction. What’s important to keep in mind here is that, although some exceptions apply, the first money you receive from an exchange (up to the amount of capital gain) shall be deemed boot and therefore taxable to you.

“Mortgage boot” becomes an issue when the debt on the Replacement Property you buy is less than the mortgage debt on the Relinquished Property you are selling. As a general rule, if the debt on the Replacement Property is not equal to or greater than the debt on the Relinquished Property, you'll have what is called “overhanging debt,” and the difference will be taxable.

For example, let’s say that you are selling your Relinquished Property for $875,000, which has a mortgage of $750,000. At closing, the mortgage will be paid off and the balance of $125,000 will be held by your Qualified Intermediary. Suppose that you then find a new property costing $850,000, with a mortgage of $725,000 that you will assume. The assumption of the $725,000 debt, along with your exchanged funds of $125,000 will complete your purchase. Under this example you would have to pay tax on $25,000 of capital gains because your debt decreased by that amount.

There are two common methods to avoid the mortgage boot problem. First, you could have the seller of the Replacement Property refinance with you assuming the new, higher debt (or you could finance it, either through a new loan or a land-sale contract). Second, you could add cash to the deal; cash "added in" offsets debt relief on the property you are selling.

Although there are too many specific rules involved with offsetting boot calculations for us to cover within this article, you should note that you may offset mortgage boot with cash, but may not offset cash boot with additional debt. Extending the previous example, you could add $25,000 of cash to offset the mortgage boot, but if you had $875,000 worth of net equity in your Relinquished Property (no debt) and exchanged into the Replacement Property with only $850,000 of equity, you would have received $25,000 in cash, which cannot then be offset with a larger loan.

To illustrate the discussed issues surrounding boot, we have provided the following three additional examples for your review:

Relinquished Property | Replacement Property | ||

$700,000 | Sale Price | $725,000 | Sale Price |

$400,000 | Debt Owed | $425,000 | Debt Assumed |

$300,000 | Equity | $300,000 | Equity |

This example depicts a fully tax deferred exchange. The new mortgage balance on the purchased property is of equal or greater value, and the equity has moved across.

Relinquished Property | Replacement Property | ||

$700,000 | Sale Price | $725,000 | Sale Price |

$400,000 | Debt Owed | $475,000 | Debt Assumed |

$300,000 | Equity | $250,000 | Equity |

In this example there is taxable boot. All of the equity is not used in acquiring another property. Any cash the exchanger puts into his pocket is taxable as "boot" (in this case, $50,000).

Relinquished Property | Replacement Property | ||

$700,000 | Sale Price | $675,000 | Sale Price |

$400,000 | Debt Owed | $375,000 | Debt Assumed |

$300,000 | Equity | $300,000 | Equity |

In this example there is also taxable boot. A property of less value was purchased, and there is a new mortgage of less value than the mortgage on the Relinquished Property. The difference between the two mortgages is classified as "mortgage relief," and is taxable as mortgage boot (in this case, $25,000).

Thus, in order to fully defer state and federal capital gain taxes, you must reinvest all exchange proceeds (to avoid cash boot) and either acquire property with equal or greater debt or reinvest additional cash equal to the debt relief (to avoid mortgage boot). Remember: you must end up with at least as much debt on the new real estate as you had when the exchange began (or replace the debt with additional cash).

Capital Gain Tax → To calculate your capital gain tax, multiply the capital gain by your combined tax rates (federal and state). Although you should confirm the current tax rates prior to beginning the calculation, for purposes here, we shall assume a federal capital gain rate of 15% and a state (e.g., South Carolina) rate of 4%. For example, multiplying a capital gain amount of $480,000 by 19% yields $91,200 in tax – either paid to the government or saved using a §1031 exchange.

For your convenience, you may use the following format to determine the amount of capital gain taxes you will either pay to the government or defer using a §1031 exchange:

$ | ____ | Cost Basis in Relinquished Property | ||

+ | $ | ____ | Capital Improvements | |

– | $ | ____ | (Depreciation Deductions) | |

$ | ____ | Adjusted Basis | ||

____ | ||||

$ | ____ | Contract Sales Price (Relinquished) | ||

– | $ | ____ | (Adjusted Basis) | |

– | $ | ____ | (Expenses & Closing Costs) | |

$ | ____ | Capital Gain | ||

____ | ||||

____ | % | Federal Capital Gain Tax Rate (15%) | ||

+ | ____ | % | State Capital Gain Rate (4% SC) | |

____ | % | Combined Capital Gain Rate (19%) | ||

____ | ||||

$ | ____ | Capital Gain | ||

x | ____ | % | Combined Capital Gain Rate | |

$ | ____ | Combined Capital Gain Tax | ||

Advantages & Disadvantages: The obvious reason for exchanging investment or business property, instead of selling it, is to avoid the immediate capital gains tax on your profit. Other advantageous motives to exchange include:

minimizing or eliminating the need for new mortgage financing on the property acquired;

stacking your investment property equity without tax erosion of your sale profits;

acquiring more desirable property or a property that better meets your investment or business needs;

increasing your depreciable basis;

avoiding the 25% depreciation recapture tax when selling an investment or business property;

refinancing either property before or after (but not during) the exchange to take out tax-free cash;

accepting a desirable purchase offer to sell a property and to avoid capital gain tax; and

avoiding capital gains tax on Replacement Properties retained at your death (the basis in most taxpayers property is increased to the fair market value of that property at their date-of-death).

In evaluating whether you should consider a §1031 exchange, you should also become familiar with some potential disadvantages, such as:

You will have a reduced basis in your Replacement Property because the basis of your Relinquished Property carries forward. Thus, whenever you decide to sell, rather than exchange, property obtained in an exchange, the capital gain will include the appreciation of all of your former Relinquished Properties.

Considerable time, energy, and money will be lost if a §1031 exchange fails. Thus, retaining the services of experienced professionals, such as Bradshaw & Company, LLC, is critical to ensuring that your exchange is structured and executed with precision.

Along these lines, a §1031 exchange involves increased transactional costs, which may include attorney’s fees, accounting fees, and the intermediary’s and accommodation titleholder’s fees.

You may not (without tax consequences) use any of the net proceeds from the sale of your Relinquished Property for anything other than reinvesting in more real estate.

FAQs:

If I am considering a §1031 exchange, what should I do initially? First, we strongly urge you to call us. With no obligations to you, an attorney at Bradshaw & Company, LLC would be happy to discuss the appropriate strategy and structure of a §1031 exchange for your particular circumstance. Regardless of circumstance, however, have your Real Estate Sale And Purchase Contract refer to “[You] and or assigns” so that you may enable the QI or EAT to step into your shoes later at closing.

When is the latest point in a real estate transaction that I can decide that I want to do a §1031 exchange? Technically, anytime before you close on a parcel of property. Although not the best for the blood pressure of our attorneys, some Bradshaw & Company, LLC clients have decided that they wanted to do a §1031 exchange minutes before they began signing all of the documents at the closing table. The window of opportunity for us to structure a §1031 exchange for you is shut once you close on either the sale or purchase of a parcel of investment or business property.

Why should I use a Qualified Intermediary? In 1991, the Treasury Regulations provided certain “safe harbor” rules that – if followed – provided that the IRS would allow the exchange to qualify for tax deferral treatment. Use of a Qualified Intermediary is sanctioned as a safe harbor by the IRS. Bradshaw & Company, LLC has a long-standing professional relationship with 1031, LLC – an experienced and exceptionally professional Charleston-based Qualified Intermediary and Exchange Accommodation Titleholder.

How much must I use to purchase my Replacement Property? Your minimum down payment for a Replacement Property should be equal to or greater than the net proceeds from the sale of your Relinquished Property in order to avoid receipt of any taxable cash.

How long must I have held a parcel of property before I can use it for a §1031 exchange? There are no statutory or judicial rules providing clear guidance on this issue. The shorter you have held a parcel of property, the stronger the IRS’ case that you intended to flip it and therefore qualify as a dealer (and that the property is inventory). The longer you’ve held it, the better. One year is the unspoken rule, though two years would be even better. It all comes down to your individual tolerance for risk. Distinguishing between dealer property and investment property can prove difficult, and there are no safe harbor provisions on which to rely. The IRS reviews certain factors to determine whether the property is being held for sale to customers in the ordinary course of business, including:

Your ordinary business;

Listing the property for sale with brokers;

The number, frequency, and continuity of sales by you;

The purpose for holding the property when acquired;

The purpose for holding the property that was replenished;

The extent and nature of the transactions involved;

The extent of the improvements (if any) made to the property;

The purpose for which the property was being held when sold; and

The amount of advertising or other efforts that were used in trying to obtain purchasers for the sale of the property.

See Klarkowski v. Comm’r, T.C. Memo 1965-328, 1965 WL 1278 (T.C. 1965).

Similarly, must I hold property for a certain period after an exchange before I transfer it? As with the previous question, it all comes down to your individual tolerance for risk. One year is still the unspoken rule here, but the longer the better.

If the Relinquished Property is held in an LLC, can I exchange my membership interest in an LLC? Generally no. Although there are some sophisticated options available through the use of Delaware Statutory Trusts, interests in Multiple-Member LLCs, Corporations, or Partnerships are not qualified property eligible for §1031 tax deferred treatment. The entity itself may enter into a §1031 exchange. Depending on the goals of each member, shareholder, or partner, however, great care must be taken by your legal counsel in properly structuring such an exchange.

Can I do a §1031 exchange to purchase Replacement Property that I eventually want as my personal residence? Savvy real estate investors have tried to figure out how to make tax-deferred exchanges of their investment or business properties with the intent of eventually exchanging into their ultimate dream homes. As explained earlier, however, personal residences don't qualify for §1031 exchanges because they don’t qualify as “investment” property. If you decide to make a §1031 exchange into your ultimate dream home, such Replacement Property must be a rental at the time of the trade. Most tax advisors suggest renting it to tenants for at least 12 months before converting it to your personal residence.

Note, however, that in October 2004, Congress closed a taxpayer-friendly loophole, which had allowed an investor to move into a dream home acquired in a trade, live in it for at least 24 months and then sell it and claim the generous IRC §121 principal residence sale tax exemption (up to $250,000 for a single owner or up to $500,000 for a qualified married couple filing a joint tax return). After October 2004, for sales of a residence acquired as Replacement Property in a §1031 exchange and in order to use the principal residence exemption, the home must have been owned at least 60 months before its resale. At least 24 of those 60 months the owner must occupy the home as his or her primary residence to qualify.

What are “Tennant in Common” properties and what role do they play in the §1031 exchange? Tennant in Common property (“TIC”) is factional ownership in a parcel of real estate. A TIC Replacement Property enables the average investor to participate in the ownership of institutional type real estate with a minimum amount of investment dollars. Each co-owner receives their own deed and enjoys the same rights as a sole owner. Investing in a TIC exchange property can provide secure monthly income, stability, and appreciation, without the management burden. TICs are quickly growing in popularity nationwide, but no establish secondary market exists yet. If you would like a low risk, modest return on your investment without the hassle of managing your investment property (or if you simply cannot find an acceptable Replacement Property and do not want to pay capital gains on the sale of your Relinquished Property), then you may consider identifying a TIC for your next Replacement Property.

What are the complexities of financing my purchase of Replacement Property in a Reverse Exchange? Unfortunately, the underwriting requirements of many mortgage companies force them to be unwilling to finance the purchase of Replacement Property that will be parked with the EAT; some don’t allow the EAT to take title in your place. Bradshaw & Company, LLC, however, has professional relationships with select lenders who repeatedly finance reverse exchanges. Also, you need to consider how you will finance the acquisition of your Replacement Property without the proceeds from the sale of your Relinquished Property. You might consider obtaining funds from another source or a bridge loan. If you need assistance in obtaining such financing, please call us so that we can connect you with an appropriate, qualified lender.

What are Delaware Statutory Trusts? In August 2004, the IRS issued Revenue Ruling 2004-86, which opened the door to single entity, multi-investor structures for financed §1031 exchanges. The Ruling states that the IRS will treat ownership in a properly structured Delaware Statutory Trust (“DST”) as a direct investment in real property for purposes of a §1031 exchange, even if the DST has more than one grantor/investor. Although considerable flexibility and uncertainty surround DSTs, many real estate professionals believe that they will become the entity of choice for multi-party, financed §1031 exchange acquisitions.

Will parking title to my Relinquished Property with the EAT trigger the due-on-sale clause? Possibly. In most situations where Bradshaw & Company, LLC has had the Relinquished Property parked with the EAT, such property has been free of debt at the time of the exchange process began. If debt does exist on Relinquished Property, however, we often can negotiate with lenders to suspend the due-on-sale clause for the period of the exchange.

If I have to pay capital gains taxes eventually, why would I bother with the expense of a §1031 exchange? The answer is the time value of money. If you pay the tax today, you have less to invest for the future. By deferring the taxes as long as you can – or perhaps forever – you receive the interest on the money instead of the government. Think of it as an interest free loan from the government. It is also important to note that ultimately, you may not have to pay the capital gains taxes. You may apply the IRC §121 personal residence exclusion, so long as you observe the new subsequent holding period. You may also pass your final Replacement Properties to your spouse and children upon your death; the basis each such property you own at death generally will be increased to the fair market value at that time. Thus all that built-in gain is forgiven.

Conclusion: The above collection of FAQs is a sample of the most common questions that clients of Bradshaw & Company, LLC have asked us over the years. We hope that the answers to these selected questions will prove helpful to you. If you have questions that are not answered in this article, please do not hesitate to contact us. We would be delighted to discuss the specific options of a §1031 exchange that would be appropriate for you and your next real estate transaction.

This Newsletter is based on current law at the time written and is for informational purposes only and under no circumstances constitutes legal advice. It is important that you discuss all legal options and consequences with a qualified attorney prior to any action. Should you wish to discuss any questions with us, to schedule a consultation, or to request additional Newsletters, please call our office at (843) 795-1909 or visit our website: www.Bradshaw-Company.com.

DOWNLOAD THE May 3, 2015 NEWSLETTER HERE

Bradshaw & Company LLC

147 Wappoo Creek Drive – Suite 605

Charleston, South Carolina 29412

843.795.1909 ∙ www.Bradshaw-Company.com